Interested in buying a small business?

Subscribe to our Listing Alerts for early access to new listings.

Buying a business can be a complex and prolonged transaction. There are many elements that impact your decision on which business to buy. Knowing the tax consequences of a transaction will allow you to negotiate better and structure a good deal.

When looking at the tax consequences of buying a business, there are several factors to consider.

Please note that Beacon does not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction.

Stock vs. Asset Sale Tax Implications

A business can be bought out by either a Stock or an Asset sale. The purchaser can either buy the Assets of a business or the Stock/Ownership interests. While both are considered means of acquiring a business, they each hold distinct tax implications.

Stock Purchase Tax Implications

A buyer can directly purchase an ownership interest if the target business is operated as a C or S corporation, a partnership, or a limited liability company (LLC) that’s treated as a partnership for tax purposes.

Generally, it is more favorable to the seller when the transaction is structured as a stock sale. Especially when a business is a C corporation, the seller has a strong preference for selling stock rather than assets because it avoids the possibility of double taxation. Since the seller's earnings from a sale are almost always treated as capital gains, stock sales qualify them for a preferential tax rate (currently 20% for 2021).

Outside of the tax implications, there are other risks a buyer in a stock transaction should consider:

Asset Purchase Tax Implications

As a buyer, in almost every instance, making an asset purchase will benefit you in regards to Tax Implications if the proper steps are taken.

To reduce the sales tax on the asset sales of businesses, buyers should make sure to inform their state’s taxing authority to give them a final opportunity to collect any pending sales taxes from the seller.

From a tax standpoint, if the company is a corporation, the buyer will benefit from structuring the transition as a purchase and sale of the company’s assets rather than buying the stock of the company. This allows the buyer to write up the tax bases of the company’s assets and thereby report greater depreciation and amortization deductions and smaller amounts of gain on re-sales of the purchased assets.

Additionally, in an asset sale, the company is selling, and the buyer is buying the company’s various assets separately for allocable portions of the aggregate purchase price.

This allows the buyer to allocate as much purchase price as possible to assets that are eligible for bonus depreciation or that are likely to turn over in the short term.

There is also another way for the buyer to purchase a business through an Asset sale.

Under Section 338 of the US tax code, if the company is an S corporation and its stockholders sell at least 80% of the outstanding stock of the company (in a single transaction or a series of transactions in a 12 month period), the sale will be treated as a sale of the company’s assets for any tax purposes. This benefits the buyer as they gain all the tax advantages that they would have when purchasing as an asset sale. Section 338 can also help expedite a direct asset purchase for buyers as well as sometimes help them acquire a business for cheaper. Since only 80% of the stock is required to institute Sec. 338, a buyer could, in theory, step up 100% of the assets by only purchasing 80% of the target’s stock.

For example:

Business X has been on the market for longer than expected, and the stakeholders now want to sell the business right away. This is when Section 338 would be used. Because Section 338 gives the buyers a tax advantage, Business X becomes more valuable and attractive, leading to a quicker sale. To balance some of the losses the incurred to sellers due to the tax disadvantage of Section 338, some sellers may also increase the asking price for their business.

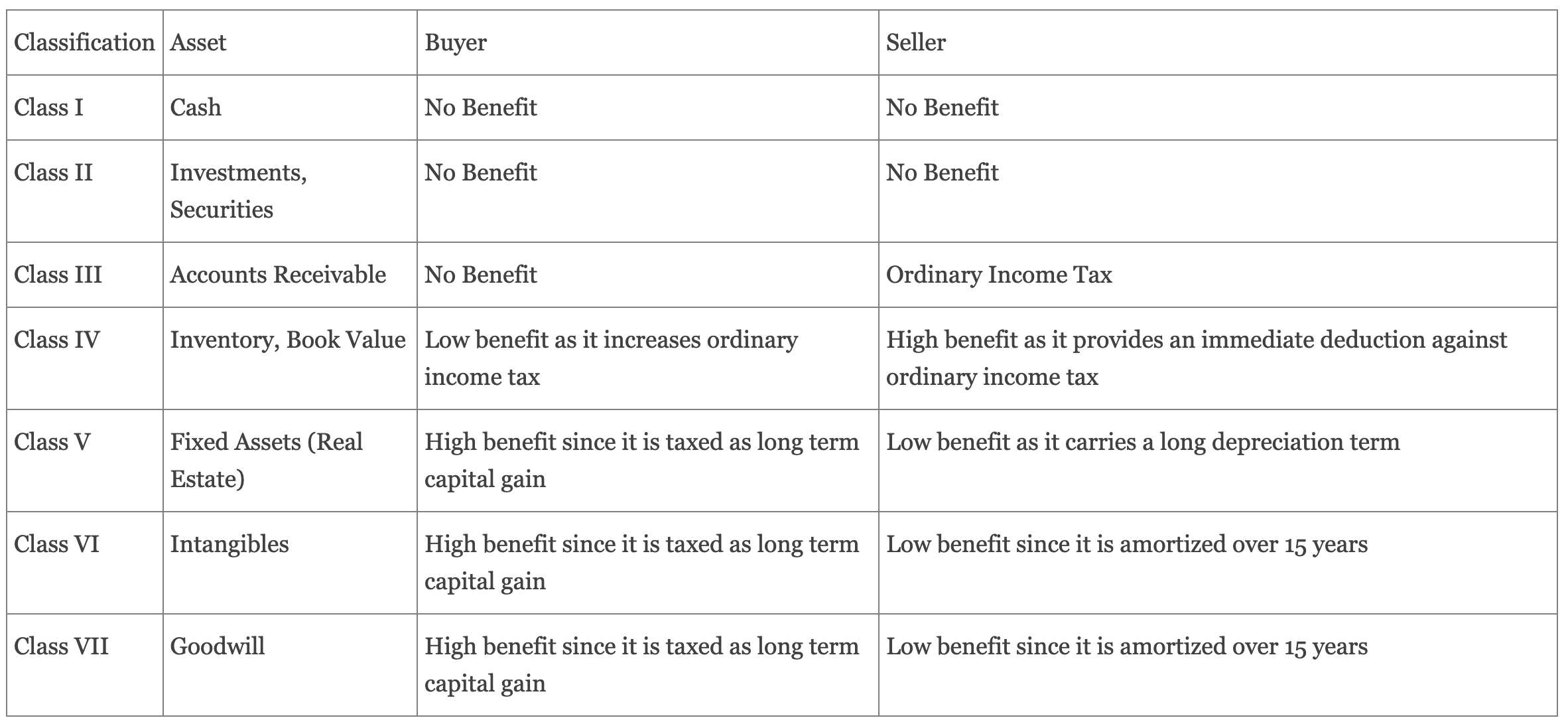

Allocations of The Purchase Price In An Asset Sale

As you buy a business, you will come across many areas where a compromise between the buyer and the seller is necessary. One such area is the tax implications that come with the allocations of the purchase price.

The IRS has divided these allocations into seven classifications. The breakdown below shows which classifications are more beneficial for buyers versus sellers.

Is Buying a Business Tax Deductible?

Yes. The IRS allows a buyer to get a tax deduction of up to $5,000 when you spend under $50,000 to buy a business. However, once you go over $50,000, your reduction threshold gets much lower. If you spend $53,000 to buy the business, then you can only deduct $2,000. If you spend anything over $55,000 to buy your business, you are no longer eligible for a deduction.

Despite relatively low thresholds for tax deductions from a sale, you can still file things such as research, travel, and training you invest in before you purchase the business as a business expense.

Seller Financing & Its Tax Benefits

Seller financing is a method that allows business buyers to bridge the gap between the down payment, conventional financing, and the asking price. It also aligns incentives for both buyers and sellers. We recommend that sellers finance between 10 and 15% of the transaction price so that the seller has some skin in the game. Many lenders will require the seller to finance at least 5% of the transaction.

In seller financing, the seller agrees to carry a note, and the buyer makes regular payments to the seller with interest. Usually, seller financing is done with a combination of other forms of financing; however, in some cases, it can be done as the sole method if a significant down payment is offered.

Benefits for Buyers

Seller financing allows the buyer to have better access to capital, better terms, and faster closing times. For small transactions, it may open up the pool of potential buyers as the fees from conventional financing may not be worth it given the size of the deal. The lowest financing rates when financing through an SBA loan usually ranges anywhere from 7.25 to 9.75%. Seller financing is completely negotiable but can often go as low as 6%. Additionally, these financing details and paperwork can be processed much quicker than with traditional financing means, as normally it’s just a matter of legal counsel drafting a satisfactory promissory note.

Benefits for Sellers

Seller financing can be attractive for sellers due to their faster closing times, attractiveness to buyers, ability to get a higher selling price, and tax benefits. However, the seller is taking the underwriting risk by acting as the “bank” to the buyer. We recommend sellers only finance in three scenarios: (1) it’s mandated by a conventional or SBA lender, (2) the buyer is putting forth a material down payment, or (3) the deal is so small that there are no other options.

Seller financing splits the payments to a seller on a monthly basis for several months or years. Receiving these drawn-out payments and reporting incremental gains as opposed to a large lump sum can lower income taxes. A seller may even structure financing to defer payments and associated gains until a tax-advantaged year.

Interested in buying a small business?

Subscribe to our Listing Alerts for early access to new listings.

Robin is a community manager and content writer at Beacon. He is a sophomore at Virginia Tech's Pamplin College of Business, double majoring in Finance & Philosophy, Politics, and Economics.

Information posted on this page is not intended to be, and should not be construed as tax, legal, investment or accounting advice. You should consult your own tax, legal, investment and accounting advisors before engaging in any transaction.

Calder Capital

Sam Domino