Not quite ready to sell?

Subscribe to receive the latest resources for small business owners.

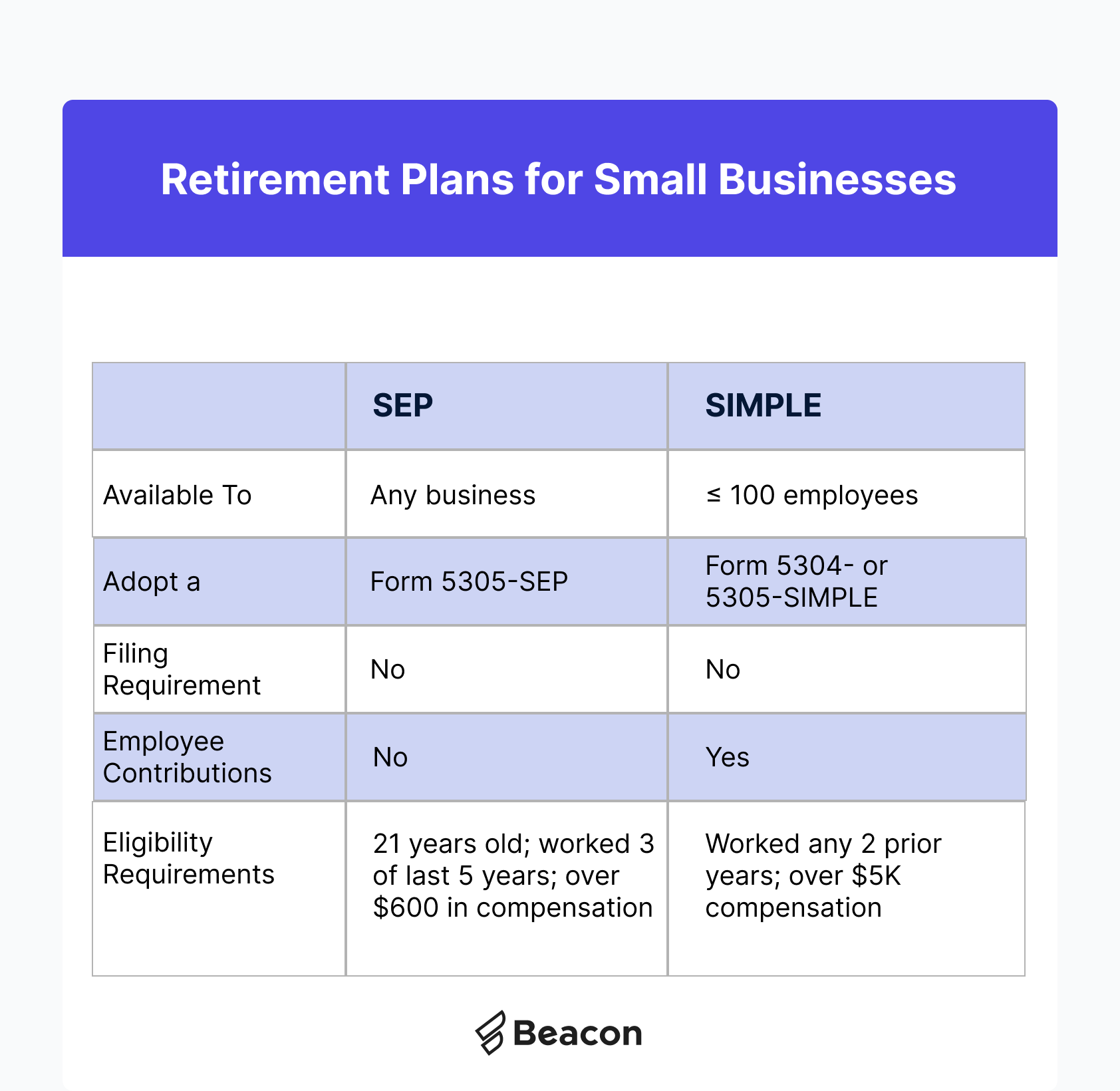

Small business owners often face a variety of challenges when it comes to offering retirement benefits to their employees and planning for their own retirement. The two common retirement plans that are available to small businesses are Simplified Employee Pension (SEP) plans and Savings Incentive Match Plan for Employees (SIMPLE) plans.

While both plans are designed to provide a simple and cost-effective way for employers to offer retirement benefits to their employees, they differ in a few key ways. In this blog post, we'll explore the differences between SEP and SIMPLE retirement plans and help you determine which plan might be best for your small business.

SEP Retirement Plans

A SEP plan is a type of employer-sponsored retirement plan that allows employers to make contributions to a traditional IRA (individual retirement account) on behalf of their employees. SEP plans are relatively easy to set up and administer, making them a popular choice for small businesses. Under a SEP plan, employers can contribute up to 25% of an employee's compensation (up to a maximum of $61,000 in 2021) to the employee's traditional IRA. The contributions are tax-deductible for the employer and tax-deferred for the employee until they withdraw the funds in retirement.

One of the key benefits of a SEP plan is that it allows employers to contribute to their own retirement accounts as well as their employees' accounts. This can be a valuable benefit for small business owners who are looking to save for retirement while also attracting and retaining talented employees.

SIMPLE Retirement Plans

A SIMPLE plan is another type of employer-sponsored retirement plan that is designed specifically for small businesses with fewer than 100 employees. SIMPLE plans are similar to 401(k) plans, but they have lower contribution limits and less administrative complexity. Under a SIMPLE plan, employers can choose to either make a matching contribution (up to 3% of an employee's compensation) or a non-elective contribution (a flat 2% of each employee's compensation, regardless of whether the employee contributes to the plan).

One of the key benefits of a SIMPLE plan is that it is designed to be easy and cost-effective to set up and administer. Employers are not required to file annual reports with the IRS, and employees can contribute to the plan directly from their paychecks. Additionally, employees are immediately vested in all employer contributions, which means that they are entitled to the full value of the contributions, regardless of how long they have been with the company.

Which Plan Is Right for Your Small Business?

When it comes to choosing between a SEP plan and a SIMPLE plan, there is no one-size-fits-all answer. Each plan has its own advantages and disadvantages, and the right choice will depend on your specific business needs and goals.

If you are a small business owner who wants to maximize your own retirement savings while also providing a valuable benefit to your employees, a SEP plan may be the right choice for you. SEP plans allow for higher contribution limits and are relatively easy to set up and administer, making them a popular choice for small business owners.

The added benefit of a SEP is that you can adjust your employer contributions based on the cash flow or earnings you have in a given year.

On the other hand, if you are looking for a simple and cost-effective way to provide retirement benefits to your employees, a SIMPLE plan may be a better choice. SIMPLE plans are designed to be easy to set up and administer, and they offer immediate vesting of employer contributions, which can be a valuable benefit for employees.

Aside from profit sharing agreements or contributing stock to employees, retirement plans are one of the best retention tactics that we see in small businesses. With more than half of the American working population lacking access to retirement plans, helping your employees save for the future is a great way to stand out.

Not quite ready to sell?

Subscribe to receive the latest resources for small business owners.

Sam is an exit planning expert, combining years of experience working with small business owners with extensive knowledge of traditional and SBA financing.

Information posted on this page is not intended to be, and should not be construed as tax, legal, investment or accounting advice. You should consult your own tax, legal, investment and accounting advisors before engaging in any transaction.

Calder Capital

Sam Domino